SP500 LDN TRADING UPDATE 11/3/26

SP500 LDN TRADING UPDATE 11/3/26

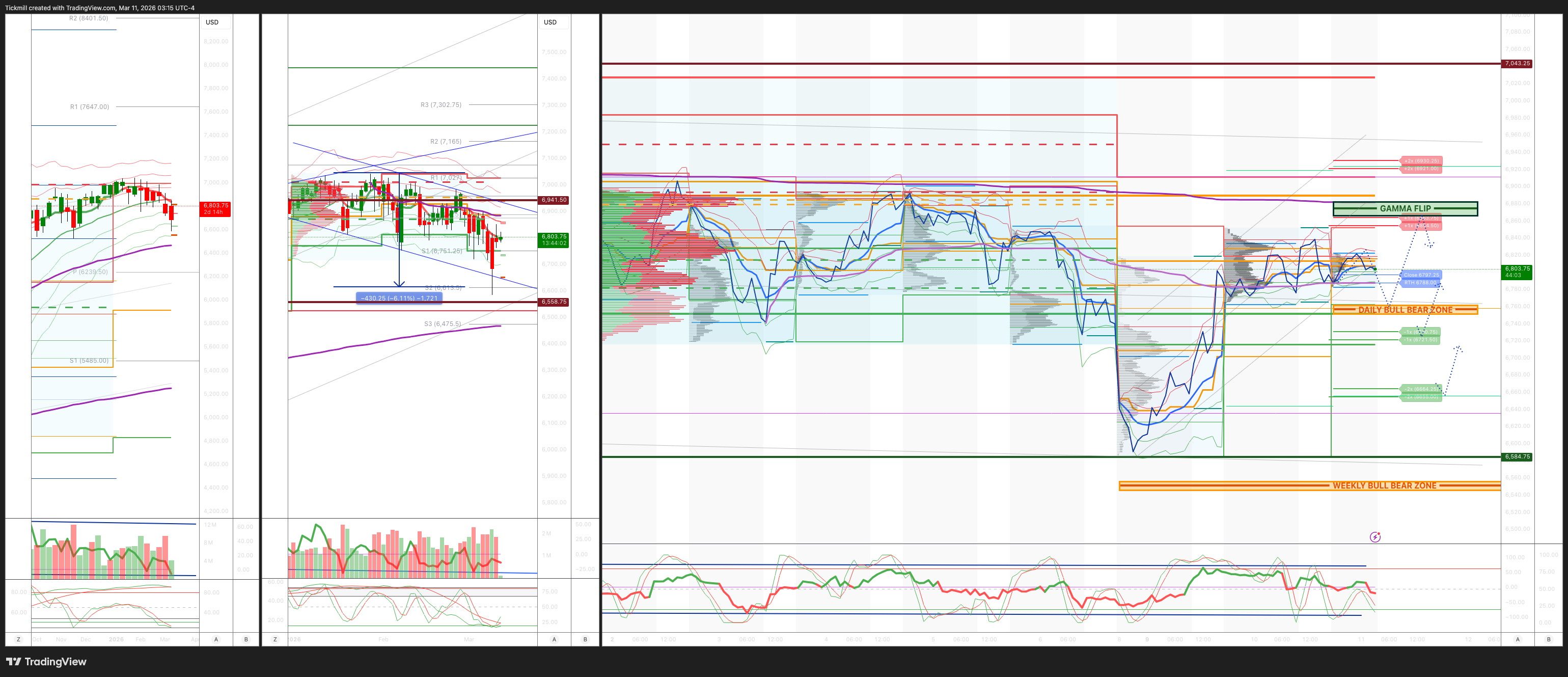

WEEKLY & DAILY LEVELS

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 6560/50

WEEKLY RANGE RES 6942 SUP 6558

Weekly Straddle Range: 192 -point straddle implies a weekly range of [6558, 942]; monitor 1.5x and 2x moves for key reactions.

March OPEX Straddle: 232.8-point range suggests OPEX-to-OPEX movement between [6677, 7142].

March QOPEX Straddle: 368.55-point range projects [6466, 7203], based on December OPEX.

March EOM Straddle: 255.4-point straddle indicates a monthly range of [6623, 7101]. .

DEC2025 to DEC2026 OPEX straddle spans 945 points, outlining a range of [5889, 7779]."

DAILY VWAP BEARISH 6793

WEEKLY VWAP BEARISH 6868

MONTHLY VWAP BEARISH 6889

DAILY STRUCTURE – BALANCE - 6641/6877

WEEKLY STRUCTURE – OTFD - 6911

MONTHLY STRUCTURE - OTFD

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFD): This describ@es a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 6750/60

GAMMA FLIP 6882

DAILY RANGE RES 6855 SUP 6721

2 SIGMA RES 6921 SUP 6655

VIX BULL BEAR ZONE 20

PUT/CALL RATIO 1.22 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

TRADES & TARGETS

LONG ON REJECT/RECLAIM OF DAILY BULL BEAR ZONE TARGET DAILY RANGE RES

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Reversal’

SPX closed down 21bps at 6,782, with a MOC of $740M to buy. NDX dipped 4bps to 24,956, R2K fell 22bps to 2,548, and the Dow dropped 7bps to 47,707. Total trading volume across U.S. equity exchanges reached 19.73 billion shares, slightly above the YTD daily average of 19.65 billion. The VIX declined 224bps to 24.93. WTI Crude tumbled 8.53% to $86.64, while the U.S. 10YR yield rose 5bps to 4.15%. Gold gained 115bps, closing at $5,197, the DXY slipped 26bps to 98.91, and Bitcoin advanced 1.81% to $70,215.

Markets experienced sharp swings as geopolitical developments dominated headlines. Trump’s statement that the war could end "soon" was followed by Hegseth asserting that the U.S. "won’t end the war until the enemy is defeated." Additional updates included reports of the U.S. Navy successfully escorting an oil tanker through the Strait of Hormuz and U.S. intelligence detecting potential Iranian efforts to deploy mines in the shipping lane.

Activity on the trading floor was subdued, rated a 3 on a 1-10 scale. The floor ended the day at -256bps for sale, compared to a 30-day average of +71bps. Momentum showed signs of stabilization, with GS Momentum Pair up 4%, driven by gains in momentum longs and declines in momentum shorts. Activity remains tilted toward ETFs and indices, with limited single-stock action. Right-tail squeeze risk appears elevated. No specific catalyst emerged for the widening gap between semiconductors and software, though factors like AVGO earnings, NVDA’s upcoming GTC conference, and global memory stabilization supported semis. Software saw a bid for covering, with GS Prime noting significant tech de-grossing last week, particularly in software, after a ~20% rebound from the Citrini low.

Post-market, ORCL surged 7% following a strong beat on cloud infrastructure revenue ($4.9B vs. $4.74B consensus) and robust overall revenue growth. Guidance was also upbeat, with Q4 total revenue expected to grow 18-20% y/y (cc) and cloud revenue projected to increase 44-48% y/y (cc). FY27 guidance was also raised.

In financials, defensive exchanges (CBOE, ICE, CME, TW) came under pressure despite the market’s overall decline. Crowding dynamics have played a role over recent weeks, potentially tied to headlines about prediction markets offering index options.

On the derivatives front, the session was marked by choppy trading, with the SPX briefly touching its 100-day moving average. Geopolitical news kept volatility elevated, leading to an inverted VIX futures curve. Skew eased significantly after the morning rally, and there was a notable break in recent patterns as investors refrained from adding hedges despite the drop in volatility. Flows showed interest in term structure buying within the index space. Looking ahead, the February CPI report is due tomorrow, with the market pricing in a 1.13% move by the close.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!