Institutional Insights: Goldman Sachs US Flow Themes

US Flows / Themes — July 6, 2026

The shortened week produced a constructive index tape but a much more violent rotation under the surface. The S&P 500 rose 1.76%, the Nasdaq Composite gained 2.12%, and the Russell 2000 slipped 0.46%, despite touching fresh record highs. The primary macro catalyst was the softer June payrolls report, which reduced immediate Fed hike concerns and pulled year-end hike pricing down to roughly 28bps from around 40bps after the June FOMC. That gave equities a rates-relief impulse into July and helped megacap tech rebound.

But the local trading narrative clearly shifted. The tape moved away from first-half AI infrastructure winners and back toward mega-cap tech and software. The SOX fell 4.4% on the week, while Apple +8.8%, Alphabet +6.7%, Meta +5.9%, and Microsoft +4.7% led the market higher. This is the same broadening / rotation theme that has been developing since quarter-end: the index remains supported, but the crowded AI bottleneck and momentum winners are being used as funding sources.

---

# 1. Macro: Softer NFP Supports the Tape, Geopolitics Recedes

The June employment report was soft at the headline level. Payrolls rose only 57k, below consensus around 110k–113k, and April/May payrolls were revised down by a combined 74k. The unemployment rate unexpectedly fell to 4.2%, but that was largely due to a drop in labor-force participation to 61.5%, not a clean sign of labor-market strength.

The market read was dovish. The report effectively removed the risk of an imminent July hike and reduced year-end hike pricing to +28bps, from +40bps as recently as June 21. For equities, this matters because the market can now enter earnings season with less immediate policy pressure. Lower hike odds support duration-sensitive growth, software, housing, real estate, and quality cyclicals.

Geopolitical risks also moved further into the background. Shipping through the Strait of Hormuz appears to be recovering faster than expected, and WTI fell 0.8% on the week back toward pre-war levels. Technical talks in Switzerland on Lebanon de-confliction, nuclear inspections, and frozen assets remain important, but for now the market is no longer pricing a major immediate energy shock.

The caveat is that crude relief does not eliminate the LNG/storage issue in Europe or refined-product tightness globally. But from an equity-index perspective, lower oil and lower hike pricing were enough to keep the risk-on tone intact.

---

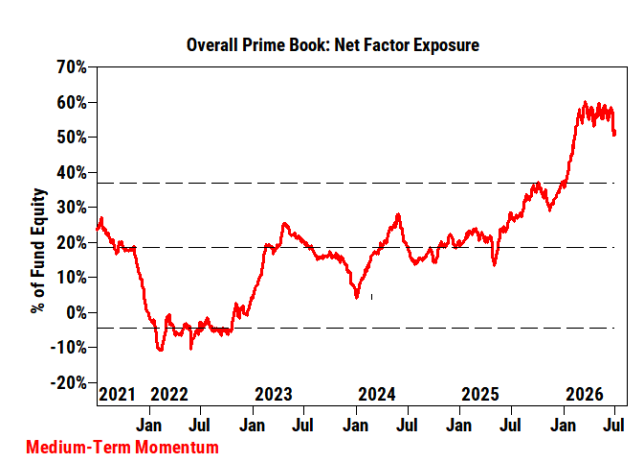

# 2. Positioning: Index Up, Hedge Fund Alpha Down

The most important point from GS Prime is that hedge funds had a challenging week even as the headline market rose. This is the clearest evidence that the current move is a factor rotation, not simple risk-on.

Key factor moves over the last five trading sessions:

- High Beta Momentum: -11.6%

- High Beta TMT Momentum: -15.8%

- US software vs semis: software outperformed semis by 12.5%

That is a painful setup for funds long AI infrastructure winners and short software / laggards. The GS Equity Fundamental L/S Performance Estimate fell 1.53% between June 26 and July 2, while the Systematic L/S estimate fell 2.09%, driven by -2.30% alpha from short-side losses.

The short-side losses are important. This suggests that the pain is not simply long AI winners going down; it is also shorts in laggards rallying. That is exactly what a broadening trade looks like from a long/short perspective.

Prime books saw net selling overall for a third consecutive week, largely driven by Asia. Tech was the most dollar net sold sector for a fourth straight week, despite being up 88bps on the week. Net selling in Tech registered -2.7 standard deviations on a one-year basis and was driven by both long and short sales at a 2.2-to-1 ratio, led by Semis & Semi Equipment and Tech Hardware.

The market has not abandoned tech; it is reallocating within tech. Semis/hardware are being sold, while software and megacap platforms are recovering.

---

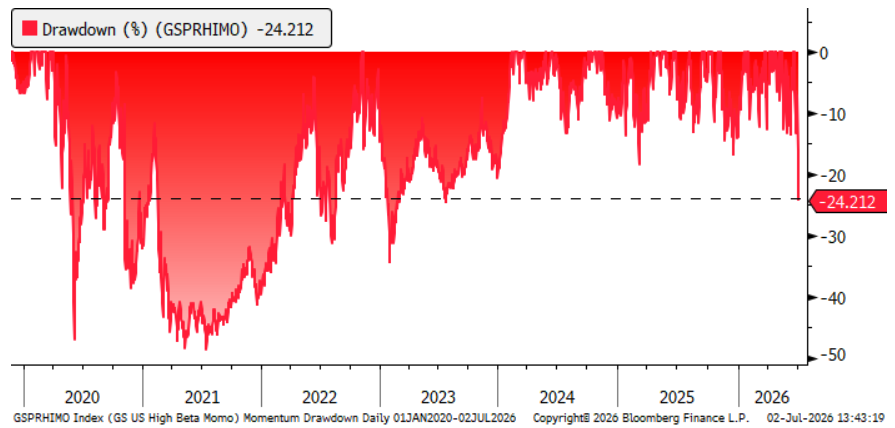

# 3. Momentum: Tactical Bounce Possible, But Crowding Still a Risk

The momentum selloff has been severe. Unconstrained momentum is now down 24% from its peak, the worst drawdown since Q1 2023. The average momentum drawdown since Covid has been around 12% over 24 days. The current episode is already twice the average drawdown and has unfolded in only 10 days.

That creates a two-sided setup.

## The Bullish / Tactical Bounce Case

- Momentum has already fallen significantly.

- Two-day 10%+ drawdowns are not unprecedented in 2026.

- Lower liquidity and holiday timing likely exaggerated the move.

- There are nascent signs of dip-buying.

- The AI story has not changed enough to justify a full factor collapse.

- Historically, absent regime change, buying momentum dips has paid off.

A tactical bounce in momentum would be consistent with prior 2026 drawdowns.

## The Bearish / Regime-Risk Case

- Momentum remains extremely crowded despite the drawdown.

- The factor is still up 27% YTD.

- The worst historical drawdown for the factor is around 50%, roughly twice the current episode.

- If there is a real fundamental shift in AI capex, ROI, or margin assumptions, the floor is much lower.

- Realized volatility for the pair is at the highest level in five years.

The right conclusion is not that momentum must keep falling, but that the risk/reward is no longer one-way. A tactical bounce is plausible, but crowding and high realized volatility mean the factor should be traded with defined-risk structures rather than large unhedged exposure.

---

# 4. AI / Corporate Developments: Platform Winners Reasserting

AI remained front and center in single-name news.

Key developments:

- Meta +5.9% on reports it may sell excess compute.

- Anthropic saw Commerce Department export restrictions lifted on Claude Fable 5 and Mythos 5.

- OpenAI reportedly discovered inference optimizations that materially lower model-running costs and proposed giving the US government a 5% stake.

- SMCI -11.1% after reports of office raids tied to an AI chip-smuggling investigation.

- MSFT +4.7% ahead of reported job cuts affecting thousands of roles.

The Meta and OpenAI developments are especially relevant to the AI capex ROI debate. If platforms can monetize excess compute or materially lower inference costs, that supports the hyperscaler/platform side of the AI ledger. It also challenges the idea that all value must accrue to bottleneck suppliers forever.

This is consistent with the recent rotation: investors are moving back into hyperscalers and software while taking profits in semis/memory/hardware.

Outside AI, consumer and non-TMT earnings were mixed but not disastrous:

- Nike +8.2%: better results, though backdrop remains challenged.

- STZ -6.0%: solid results but market reaction weak despite reiterated FY27 guidance.

- GIS +4.3%: beat, aided by pricing and mix margin benefits.

- FDS +7.9%: better earnings and organic ASV growth.

The consumer read-through remains selective rather than uniformly strong or weak.

---

# 5. Week Ahead: Quiet Macro, But FOMC Minutes Matter

The macro calendar is lighter, but not empty.

Key events:

1. Monday — June ISM Services

- GS expects a decline to 54.0 from 54.5.

- Still expansionary, but any downside surprise would matter after soft NFP.

2. Wednesday — FOMC Minutes

- The market will scrutinize assumptions behind the hawkish June projections.

- Key question: how strongly did participants lean into hikes, and what inflation/growth assumptions drove that?

3. Fed Speakers

- Waller on Monday

- Williams and Logan on Thursday

After the soft jobs report, any indication that the Fed is less committed to further hikes would reinforce the bullish July setup. Conversely, if the minutes or speakers defend the hawkish dots too aggressively, rate volatility could return.

Micro calendar is quiet ahead of the official Q2 earnings kickoff on July 14.

Notable prints:

- LEVI Wednesday evening

- PEP Thursday morning

- DAL Friday morning

- H Friday morning

Investor / analyst days:

- CPRT

- ZETA

- CLMB

- VERI

- AVAV

---

# 6. Small Caps: Strong H1, But H2 Upside Looks More Limited

Small caps have been a major positive surprise. The Russell 2000 returned 23% in H1 and 41% over the past 12 months, roughly doubling the S&P 500 return on both a 6- and 12-month basis. But this only reverses a small portion of the past 15 years of underperformance: the S&P 500 has generated roughly 680% total return versus 375% for the Russell 2000.

The AI trade has been a major contributor. Before the recent rebalance, semiconductors and GS AI infrastructure constituents represented 15% of Russell 2000 weight and 37% of its YTD return. AI infrastructure stocks contributed roughly 40% of Russell 2000 YTD performance.

But the recent reconstitution changes the forward setup. The weight of AI infrastructure stocks in the Russell 2000 has fallen from 15% to 7%, removing some of the largest YTD contributors. That reduces the AI tailwind for small caps in H2.

The earnings outlook is very strong on paper. Consensus expects 48% Russell 2000 EPS growth in 2026, roughly twice the S&P 500 growth rate. If realized, that would be one of the strongest years in decades outside 2009 and 2021. But revisions are a concern: Russell 2000 2026 EPS estimates have been cut 9% YTD, while S&P 500 estimates have been raised 9%.

That means the Russell 2000 rally has been split between earnings growth and multiple expansion, whereas the S&P’s YTD gain has been entirely earnings-driven. With the Russell trading at 2.4x P/B, above its long-term average of 2.1x and above the 2.2x start-of-year level, valuations are less compelling.

The H2 view is therefore more cautious: elevated valuations plus near-trend growth point to low-single-digit returns over the next 12 months. Key risks are disappointing growth and a hawkish Fed, especially because 29% of Russell 2000 debt is floating rate versus 7% for the S&P 500, and nearly 30% of constituents are unprofitable.

Bottom line on small caps: the rally has been impressive, but the easy AI/rebalance-driven outperformance may be behind us. Selectivity matters more now.

---

# 7. Semis Preview: Broad Upside, But Bar Is Higher

Jim Schneider expects broad upside in semis into Q2 earnings, but acknowledges that the first-half run has raised the bar. The opportunity set is increasingly stock-specific.

Key views:

## AMD: Tactical Buy

AMD is favored tactically due to:

- Upside to server CPU demand,

- Increasing AI attach,

- Quantification of the MI450 ramp in 2H,

- New customer engagement commentary,

- Potential upward pressure on 2027 data-center estimates.

The GS 2027 EPS estimate of $14.50 is 13% above Street, which supports upside if management commentary validates the data-center trajectory.

## Memory / Storage: Prefer HDDs and NAND Over DRAM

There is less fundamental upside for the broader memory/storage complex after the massive run. However, HDDs and NAND are preferred due to limited incremental near-term supply additions.

In DRAM, the more attractive expression may be equipment rather than memory producers. AMAT is viewed constructively, with focus on potential upside to CY26 WFE in 2H, driven by memory/foundry upside and early signs of CY27 acceleration.

## ARM: Highest Conviction Sell

ARM is the highest-conviction sell. The concern is that expectations are elevated after the stock’s significant run. Investors will focus on:

- Supply availability for incremental AGI CPU demand,

- Management’s prior comments about $2bn in FY27–28 AGI CPU demand,

- Additional $1bn demand constrained by supply,

- FY27 royalty revenue commentary,

- Server CPU strength versus smartphone weakness.

Given the run-up, the risk is that even positive commentary may not be enough.

---

# 8. Banks: Strong Operating Leverage, Fair Valuation

Banks enter Q2 earnings with a strong operating backdrop but fair valuations after a 17% rally in 2Q26. The group’s FY+2 P/E multiple is near the 80th percentile, and banks trade at around 65% of the S&P 500 multiple.

The top constructive ideas are:

- WFC

- BAC

- C

Three themes matter most:

## Net Interest Income

NII outlook remains strong. Analysts expect 8% NII growth in 2026, driven by:

- 9% loan growth

- Commercial lending strength, especially C&I and NDFI

- Fixed-rate asset repricing

- Industry loan growth tracking 6.1% YoY

- Deposit growth tracking 6.2% YoY

- Deposit betas declining from 52% to 48%

Even with the forward curve pricing a year-end Fed hike, the late-year timing means the 2026 NII outlook is mostly unchanged. A parallel 25bp upward shift in the curve could add 1.0% to 1.5% upside to 2027 NII and EPS.

## Capital Markets

Capital markets are a major upside lever. 2026 US IPO gross proceeds are projected to reach $225bn, an all-time high, 530% above the 2010–2025 average and 95% above the 2021 peak.

That could generate a US IPO fee pool of $4.5bn to $9.0bn, up 90% to 280% YoY. Street ECM forecasts look too conservative, currently up only around 25% YoY on average.

There is also historical linkage between ECM and equities trading during IPO spikes, with a 63% R-squared. If 2H26 equities trading declines only 10% sequentially rather than the 28% currently estimated, analysts estimate 10.5% upside to 2026 equities trading and 1.5% EPS upside.

## Expense Discipline

Large banks are showing strong expense control. Most are targeting more than 200bps of operating leverage and core efficiency ratios near 58% in 2026. Core expenses are expected to grow 7%, but core revenue growth of 11% should more than offset that, producing roughly 200bps of efficiency improvement in 2026 and another 100bps in 2027.

Credit remains benign, with net charge-offs expected stable around 55bps.

Bottom line on banks: valuations are no longer cheap, but earnings quality, operating leverage, NII, capital markets, and benign credit support continued ownership, particularly in BAC, C, and WFC.

---

The market’s message is increasingly clear: the index can keep working even as first-half leadership rotates.

The shortened week was bullish at the S&P/Nasdaq level because soft payrolls reduced Fed hike risk and megacap tech rebounded. But beneath the surface, hedge funds were hit by a sharp momentum unwind as AI infrastructure and semis sold off while software and mega-cap platforms recovered.

The H2 playbook remains:

- Stay tactically constructive on equities into earnings

- Expect broadening rather than one-way momentum leadership

- Add hyperscaler/software upside where positioning and valuation are attractive

- Be selective in semis after the first-half run

- Use defined-risk structures for momentum dip-buying

- Favor banks as cyclical earnings beneficiaries

- Be more selective on small caps after reconstitution reduced AI exposure

- Watch FOMC minutes and Fed speakers for confirmation that hike risk is fading

The key risk is not that the bull market has ended. The key risk is that the easiest part of the AI infrastructure/momentum trade has passed, and H2 returns will require more active rotation, tighter risk management, and better differentiation between crowded winners and newly recovering laggards.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!